Understanding Us Tax Return Calculation: A Practical Guide

For many people, filing a US tax return feels complicated and confusing. Numbers, forms, and rules can be overwhelming. But if you break down the process, tax return calculation becomes much clearer. This guide walks you through each step, using simple language and real examples.

You will learn how US tax returns work, what affects your taxes, and how to calculate what you owe or get refunded. Whether you are an employee, self-employed, or just curious, this article helps you understand US tax return calculation from start to finish.

What Is A Us Tax Return?

A US tax return is a form sent to the Internal Revenue Service (IRS) each year. It reports your income, deductions, credits, and the taxes you paid. The most common form is Form 1040. Filing a tax return is required if your income is above a certain amount.

People file tax returns to:

- Report yearly income to the government

- Claim deductions and credits

- Calculate how much tax is owed or refunded

Your tax return shows if you paid enough taxes during the year or if you need to pay more. Sometimes, you get a refund if you paid too much.

Key Elements In Tax Return Calculation

Calculating your US tax return means following a process. Here are the main steps:

- Calculate total income

- Subtract deductions

- Apply tax rates

- Subtract credits

- Compare to taxes already paid

Let’s break down each part.

Types Of Income

You must report all income sources. The most common are:

- Wages and salaries (from jobs)

- Self-employment income

- Interest and dividends

- Rental income

- Capital gains (from selling assets)

- Social Security benefits

Some income is not taxable, like gifts or certain scholarships.

Deductions

Deductions reduce your taxable income. You can choose the standard deduction or itemize your deductions.

For the 2023 tax year, the standard deduction is:

| Filing Status | Standard Deduction |

|---|---|

| Single | $13,850 |

| Married Filing Jointly | $27,700 |

| Head of Household | $20,800 |

Itemized deductions include:

- Mortgage interest

- State and local taxes

- Medical expenses

- Charitable donations

Most people use the standard deduction because it is simpler and often bigger.

Tax Rates

The US uses a progressive tax system. This means tax rates increase as income goes up. Here are the federal income tax rates for 2023:

| Tax Rate | Single | Married Filing Jointly |

|---|---|---|

| 10% | $0–$11,000 | $0–$22,000 |

| 12% | $11,001–$44,725 | $22,001–$89,450 |

| 22% | $44,726–$95,375 | $89,451–$190,750 |

| 24% | $95,376–$182,100 | $190,751–$364,200 |

| 32% | $182,101–$231,250 | $364,201–$462,500 |

| 35% | $231,251–$578,125 | $462,501–$693,750 |

| 37% | $578,126 and up | $693,751 and up |

These rates apply to taxable income (after deductions).

Tax Credits

Tax credits lower your tax bill directly. Some common credits are:

- Child Tax Credit

- Earned Income Tax Credit (EITC)

- Education Credits

A credit is more valuable than a deduction. For example, a $1,000 credit reduces taxes by $1,000.

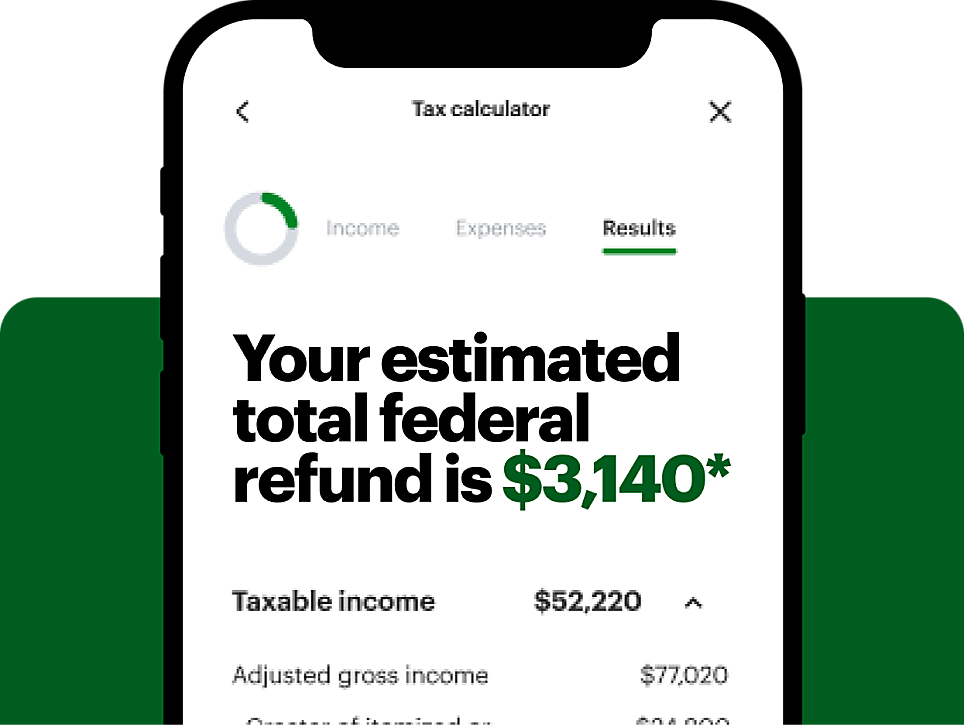

Step-by-step Calculation Example

Let’s walk through a simple example. Imagine Maria, who is single and earned $50,000 in 2023.

- Total Income: $50,000 (salary)

- Standard Deduction: $13,850 (single)

- Taxable Income: $50,000 – $13,850 = $36,150

Now, use the tax brackets:

- First $11,000 taxed at 10% = $1,100

- Next $25,150 ($36,150 – $11,000) taxed at 12% = $3,018

Total Tax Before Credits: $1,100 + $3,018 = $4,118

If Maria has a $500 tax credit:

- Final tax owed: $4,118 – $500 = $3,618

If Maria’s employer withheld $4,000 in taxes, she gets a refund:

- Refund: $4,000 – $3,618 = $382

This example shows the basic calculation for a simple return. Real returns may have more income sources, deductions, and credits.

Common Mistakes In Us Tax Return Calculation

Many people make errors when filing taxes. Here are mistakes to watch out for:

- Using the wrong filing status (Single, Married, etc.)

- Missing income sources (side jobs, bank interest)

- Forgetting deductions or credits

- Math errors

- Not checking for tax law changes

Even small mistakes can delay refunds or cause IRS problems. Double-check each step and use reliable tax software or a professional if unsure.

Comparing Standard And Itemized Deduction

Choosing between the standard deduction and itemizing is important. Here’s a comparison:

| Factor | Standard Deduction | Itemized Deduction |

|---|---|---|

| Ease | Very simple | Complex |

| Amount | Fixed | Varies |

| Best For | Most people | High expenses |

| Risk of Error | Low | Higher |

If your itemized deductions are not more than the standard deduction, use the standard.

Special Situations In Tax Calculation

Some people have special tax rules:

Self-employed

If you are self-employed, you report income on Schedule C. You also pay self-employment tax (Social Security and Medicare). You can deduct business expenses, but must keep records.

Dependents

If you support children or other people, you may claim them as dependents. This can lower taxes with credits like the Child Tax Credit.

Retirement Income

Retirement income from 401(k) or IRA is usually taxable. Social Security may be partly taxable depending on other income.

Multiple States

If you moved or worked in more than one state, you may need to file state returns for each.

Tax Software And Professional Help

Most people use tax software or hire a tax preparer. Software helps avoid mistakes and checks for credits. Popular options include TurboTax, H&R Block, and TaxAct. For complex returns (business, investments, multiple states), a professional is best.

How Refunds And Payments Work

After you file, the IRS checks your return. If you paid too much tax during the year, you get a refund. If you paid too little, you must pay the difference.

Refunds are usually sent by direct deposit or check. Payments can be made online or by mail.

The average tax refund in 2023 was around $2,900. Most refunds are processed in 21 days, but mistakes or audits can delay this.

Non-obvious Insights For Beginners

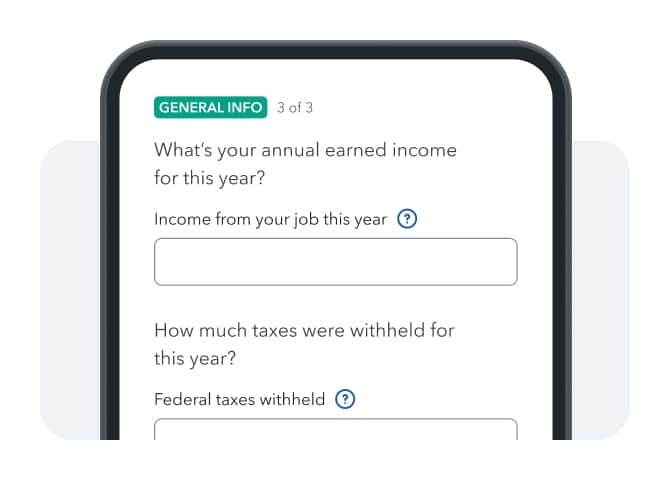

- Withholding isn’t always accurate: Your employer’s tax withholding may not match your real tax owed. If you change jobs or have side income, adjust your withholding with a new W-4 form.

- Credits can be refundable or nonrefundable: Some credits (like EITC) give you money even if you owe no tax. Others only reduce your tax bill to zero.

- Filing early helps: If you file early, you get your refund sooner and lower your risk of identity theft.

Practical Tips For Accurate Tax Return Calculation

- Keep records all year: Save pay stubs, receipts, and bank statements.

- Check IRS updates: Tax laws change often. See the IRS website for new rules.

- Use last year’s return: Compare to make sure nothing is missing.

- Review before submitting: Double-check math and spelling.

- Ask for help if needed: For complex returns, consult a professional.

Us Tax Return Calculation For Non-residents

Non-residents file Form 1040-NR. They pay tax only on US income. Deductions and credits are limited, so returns are usually simpler but sometimes less favorable.

External Resource

For official tax brackets and deduction amounts, visit the IRS site: IRS.gov

Frequently Asked Questions

How Do I Know If I Need To File A Us Tax Return?

If your income is above certain limits, you must file. Limits depend on age, filing status, and income type. For most people, if you earned more than the standard deduction, you need to file.

What Happens If I Make A Mistake On My Tax Return?

Mistakes can delay refunds or cause IRS letters. You can fix errors by filing an amended return (Form 1040-X).

Can I Deduct Expenses If I Work From Home?

Some home office expenses are deductible for self-employed people. For employees, most expenses are not deductible since tax law changes in 2018.

How Long Should I Keep Tax Records?

Keep tax records for at least three years. If you claim certain credits or have complex returns, keep records longer.

How Can I Check My Refund Status?

You can check your refund status online using the IRS “Where’s My Refund? ” tool. Most refunds arrive in about 21 days.

Getting your US tax return calculation right gives peace of mind and helps avoid problems with the IRS. With careful steps, good records, and reliable tools, you can file confidently—even if English is not your first language. Remember, tax rules change often, so always check for updates and stay informed.

Co-Founder, Owner, and CEO of MaxCalculatorPro.

Ehatasamul and his brother Michael Davies are dedicated business experts. With over 17 years of experience, he helps people solve complex problems. He began his career as a financial analyst. He learned the value of quick, accurate calculations.

Ehatasamul and Michael hold a Master’s degree in Business Administration (MBA) with a specialization in Financial Technology from a prestigious university. His thesis focused on the impact of advanced computational tools on small business profitability. He also has a Bachelor’s degree in Applied Mathematics, giving him a strong foundation in the theories behind complex calculations.

Ehatasamul and Michael’s career is marked by significant roles. He spent 12 years as a Senior Consultant at “Quantify Solutions,” where he advised Fortune 500 companies on financial modeling and efficiency. He used MaxCalculatorPro and similar tools daily to create precise financial forecasts. Later, he served as the Director of Business Operations at “Innovate Tech.” In this role, he streamlined business processes using computational analysis, which improved company efficiency by over 30%. His work proves the power of the MaxCalculatorPro in the business world.

Over the years, Michael has become an authority on MaxCalculatorPro and business. He understands how technology can drive growth. His work focuses on making smart tools easy to use. Michael believes everyone should have access to great calculators. He writes guides that are simple to read. His goal is to share his knowledge with everyone. His advice is always practical and easy to follow.