Millions of Americans invest in US savings bonds for their safety, simplicity, and government backing. But one area that often confuses both new and experienced bondholders is knowing when their bonds reach maturity—and how much they’re worth at that time. That’s where a US savings bonds maturity calculator becomes a valuable tool. If you want to get the most from your savings bonds, understanding how maturity works and how to accurately estimate value is essential.

What Are Us Savings Bonds?

US savings bonds are government-issued debt securities. When you buy one, you’re essentially lending money to the US government, which promises to pay you back with interest. They’re popular because they are low risk, easy to buy, and offer tax advantages. There are two main types: Series EE and Series I.

- Series EE bonds: These earn a fixed interest rate and are guaranteed to double in value in 20 years if held that long. They continue to earn interest for up to 30 years.

- Series I bonds: These offer a variable rate based on inflation, plus a fixed rate set at purchase. They also earn interest for up to 30 years.

Both types must be held for at least one year, and if you redeem them before five years, you lose the last three months of interest.

Why Does Maturity Matter?

Maturity is when a bond stops earning interest. For US savings bonds, that’s usually at 30 years. Knowing the maturity date is important because:

- After maturity, the bond earns nothing.

- You might miss out on interest if you redeem too early.

- Bonds must be cashed in before 30 years to avoid losing potential earnings.

Many people hold old paper bonds inherited from relatives, not realizing they might be worth much more than face value—or have already stopped earning interest.

How A Us Savings Bonds Maturity Calculator Helps

A maturity calculator is an online tool that helps you quickly see:

- The current value of your bond

- How much interest it has earned

- When it will stop earning interest (final maturity date)

- The total value at maturity

These calculators take the guesswork out of planning when to cash your bonds. They use official government formulas, and you only need basic info from your bond: series, denomination, issue date, and sometimes the serial number.

Example: Using A Maturity Calculator

Suppose you have a $100 Series EE bond issued in June 2000. If you enter these details into a maturity calculator, you’ll see:

- Issue date: June 2000

- Face value: $100

- Current value (as of June 2024): About $201.76

- Final maturity: June 2030

- Interest earned: $101.76

This quick check can help you decide if it’s time to cash your bond or keep holding it.

Where To Find A Reliable Maturity Calculator

The most trusted source is the official US Treasury website’s Savings Bond Calculator. You can access it at TreasuryDirect. Other reputable financial websites also offer calculators, but always check that the tool is up-to-date and covers the right bond series.

Key Features To Look For In A Maturity Calculator

Not all calculators are created equal. To avoid mistakes, make sure your calculator can:

- Handle both Series EE and I bonds: Some calculators only work with one type.

- Show total value at different dates: Useful if you’re planning for a future cash-out.

- Explain how values are calculated: Transparency helps you trust the results.

- Save or print reports: For record-keeping, especially when managing multiple bonds.

Below is a comparison of key features among three popular maturity calculators:

| Calculator | Series EE Support | Series I Support | Printable Reports | Direct Value Lookup |

|---|---|---|---|---|

| TreasuryDirect | Yes | Yes | Yes | Yes |

| Bankrate | Yes | No | No | Yes |

| Investor.gov | Yes | Yes | No | No |

How To Use A Us Savings Bonds Maturity Calculator

Using a calculator is straightforward. Here’s a practical step-by-step guide:

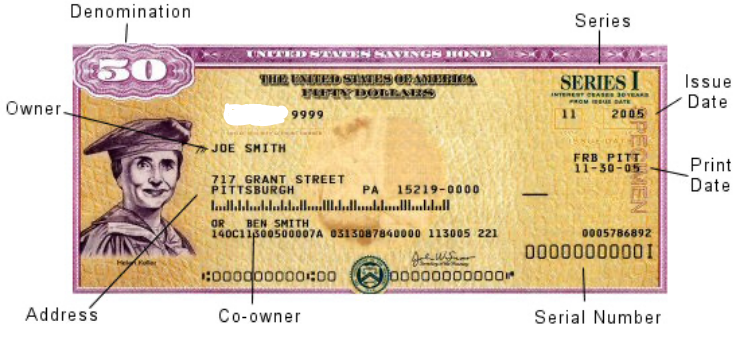

- Find your bond details: Look for the series (EE or I), issue date (month and year), and face value. For paper bonds, this is printed on the bond.

- Go to a trusted calculator: Use the TreasuryDirect tool or a reputable financial website.

- Enter your details: Select the bond series, enter the denomination, and the issue date.

- View your results: The calculator will show current value, interest earned, and maturity date.

For example, let’s say you find a Series I bond issued in April 2010, with a face value of $500. Entering this info will show you exactly how much it’s worth today, and when it will mature.

Common Mistakes When Calculating Bond Maturity

Even with a calculator, it’s easy to make errors. Here are some frequent mistakes and how to avoid them:

- Wrong bond series: Series EE and I have different rules. Double-check before entering data.

- Incorrect issue date: Enter the date as shown (month/year), not when you received or found the bond.

- Assuming all bonds double in 20 years: Only Series EE bonds issued after May 2005 are guaranteed to double in 20 years. Earlier bonds may have different rates.

- Forgetting about tax: Interest is taxable at the federal level, but not state or local.

Understanding Bond Growth: How Interest Is Calculated

Both types of savings bonds earn compound interest, but the way it’s calculated varies.

Series Ee Bonds

- For bonds issued since May 2005: Earn a fixed rate set at purchase.

- Bonds are guaranteed to at least double in 20 years.

- If the fixed rate doesn’t double the bond in 20 years, the Treasury makes a one-time adjustment.

Series I Bonds

- Earn a combination of fixed rate plus inflation rate (adjusted twice a year).

- The inflation part changes, so the total return can go up or down.

Here’s a quick comparison:

| Feature | Series EE Bonds | Series I Bonds |

|---|---|---|

| Interest Type | Fixed | Fixed + Inflation |

| Maturity | 30 years | 30 years |

| Minimum Hold | 1 year | 1 year |

| Early Redemption Penalty | 3 months interest if < 5 years | 3 months interest if < 5 years |

When Should You Redeem Your Bonds?

Timing is important. Here are some points to consider:

- Before 5 years: You lose the last 3 months of interest as a penalty.

- After 5 years but before 30 years: You can redeem at any time without penalty, but you might earn more if you wait.

- At or after maturity (30 years): The bond stops earning interest. There’s no reason to keep it after this point.

Non-obvious Insights

Many people don’t realize that:

- Matured bonds still need to be cashed. The government does not pay you automatically. Bonds that matured years ago might be sitting in your files, earning nothing.

- Paper bonds issued before 1974 may have special rules—some older bonds stopped earning interest long ago and should be checked with a calculator.

Tax Implications At Maturity

Interest from savings bonds is subject to federal tax when you redeem the bond or it matures, whichever comes first. However, you can delay reporting the interest until you cash the bond. For some, using the interest for qualified educational expenses can reduce or eliminate tax, but you must meet all requirements.

Managing Multiple Bonds

If you have several bonds, tracking them can be tricky. Most calculators allow you to enter details for multiple bonds and generate a report. For large collections, consider:

- Creating a spreadsheet with bond details and values

- Reviewing bonds annually to check for matured ones

- Assigning a trusted family member to manage bonds in case of inheritance

Digital Vs. Paper Bonds

Since 2012, the US stopped issuing paper savings bonds (except in special cases). Most new bonds are electronic, managed through TreasuryDirect. Digital bonds are easier to track, and the site provides built-in calculators and reminders for maturity.

| Characteristic | Paper Bonds | Digital Bonds |

|---|---|---|

| Purchase Method | Banks, mail (no longer available) | Online at TreasuryDirect |

| Tracking Value | Manual, with calculator | Automatic, online |

| Replacement if Lost | Paperwork required | Easy, online account |

Tips For Maximizing Savings Bond Value

- Check bonds at least once a year. Don’t let bonds sit forgotten after they mature.

- Redeem matured bonds promptly. You won’t earn more interest, and you might lose buying power due to inflation.

- Use the maturity calculator for planning. It helps you time redemptions to avoid tax surprises and maximize returns.

- Keep records of all bonds. For security and ease of tracking, especially if you own paper bonds.

Frequently Asked Questions

What Information Do I Need To Use A Maturity Calculator?

You’ll need the series (EE or I), issue date, and face value of your bond. For paper bonds, this is printed on the front. For digital bonds, check your TreasuryDirect account.

Do Savings Bonds Keep Earning Interest After Maturity?

No, savings bonds stop earning interest at final maturity, usually after 30 years. There’s no benefit to holding them longer.

Can I Cash My Savings Bond Before Maturity?

Yes, but if you cash it before 5 years, you lose the last 3 months of interest as a penalty. After 5 years, you can redeem without penalty, but you’ll stop earning interest if you cash before maturity.

Are Maturity Calculators Accurate?

If you use a reputable calculator like TreasuryDirect, the results are accurate and based on official formulas. Always double-check your bond details to avoid mistakes.

What Should I Do If I Find Old Paper Bonds?

First, use a maturity calculator to check their current value and maturity status. Some old bonds may have stopped earning interest. If they’re matured, cash them at your bank or through the US Treasury.

Getting the full benefit of your US savings bonds is all about knowing when they mature and how much they’re worth. With the right maturity calculator, you can make smart decisions, avoid costly mistakes, and be confident about your financial future. Don’t let your bonds sit forgotten—use these tools to maximize their value and achieve your savings goals.

Co-Founder, Owner, and CEO of MaxCalculatorPro.

Ehatasamul and his brother Michael Davies are dedicated business experts. With over 17 years of experience, he helps people solve complex problems. He began his career as a financial analyst. He learned the value of quick, accurate calculations.

Ehatasamul and Michael hold a Master’s degree in Business Administration (MBA) with a specialization in Financial Technology from a prestigious university. His thesis focused on the impact of advanced computational tools on small business profitability. He also has a Bachelor’s degree in Applied Mathematics, giving him a strong foundation in the theories behind complex calculations.

Ehatasamul and Michael’s career is marked by significant roles. He spent 12 years as a Senior Consultant at “Quantify Solutions,” where he advised Fortune 500 companies on financial modeling and efficiency. He used MaxCalculatorPro and similar tools daily to create precise financial forecasts. Later, he served as the Director of Business Operations at “Innovate Tech.” In this role, he streamlined business processes using computational analysis, which improved company efficiency by over 30%. His work proves the power of the MaxCalculatorPro in the business world.

Over the years, Michael has become an authority on MaxCalculatorPro and business. He understands how technology can drive growth. His work focuses on making smart tools easy to use. Michael believes everyone should have access to great calculators. He writes guides that are simple to read. His goal is to share his knowledge with everyone. His advice is always practical and easy to follow.