Choosing the right life insurance is not easy, especially if you’re in the UK and want to make sure your family is protected. You may wonder: How much cover do I need? How much will it cost? This is where a life insurance calculator UK comes in. It helps you work out how much money your loved ones might need if something happens to you, and what your monthly payments could look like. In this guide, you’ll learn what these calculators do, how they work, what affects your results, and how to use them to make smart decisions.

What Is A Life Insurance Calculator?

A life insurance calculator is an online tool that helps you estimate how much cover you should buy and how much it may cost. You enter some basic details—like your age, income, debts, and family size—and the calculator gives you a suggested cover amount. Some calculators also show you estimated monthly premiums for different types of policies.

These tools are free and easy to use. They do not give you a final quote, but they help you start the process with clear numbers. Most UK insurers and comparison sites offer their own calculators.

Why Use A Life Insurance Calculator In The Uk?

Life in the UK comes with its own set of financial needs—mortgages, student loans, and living costs that are always changing. Using a life insurance calculator UK gives you:

- Clarity: You see exactly what you might need, based on your actual situation.

- Speed: In minutes, you get a rough idea of the right cover amount.

- Confidence: You can talk to insurers or brokers with facts and numbers.

- Avoiding Over/Under-Insurance: Many people buy too much or too little cover. Calculators help you avoid these common mistakes.

How Does A Life Insurance Calculator Work?

Most calculators use a simple formula based on your answers. Here are the usual steps:

- Input Details: Age, gender, health, smoking status.

- Financial Questions: Mortgage size, debts, children’s ages, household income.

- Policy Preferences: Length of cover (term), type of insurance (level, decreasing, joint).

- Result: Suggested cover amount and sometimes estimated monthly cost.

Some calculators ask more detailed questions, while others keep it basic.

Example: Inputs And Outputs

Let’s say you’re 35, non-smoker, have a £200,000 mortgage, two children (ages 4 and 7), and £15,000 in other debts. You want cover until your youngest child turns 21.

You enter these details. The calculator may suggest:

- Cover needed: £250,000–£300,000

- Suggested policy length: 17 years

- Estimated monthly premium: £18–£25 (for a healthy non-smoker)

This is not a quote, but it helps you see what to expect.

Key Factors That Affect Your Life Insurance Calculation

Several things can change your results. Here are the most important ones:

Age

Younger people usually pay less for life insurance because they are less likely to claim soon. A 30-year-old pays much less than a 50-year-old for the same cover.

Health And Lifestyle

Health issues (like diabetes, high blood pressure), being overweight, or smoking can raise your premiums. Non-smokers often save up to 50% compared to smokers.

Policy Type

- Level term: Pays out a fixed amount if you die during the policy.

- Decreasing term: Payout reduces over time (good for covering a mortgage).

- Whole-of-life: Pays out whenever you die, but costs more.

Amount Of Cover

More cover means higher premiums. But too little means your family may struggle.

Length Of Cover

Longer policies cost more per month. But choosing a term that’s too short can leave your family unprotected.

Occupation

Some jobs (like construction) are riskier and may mean higher premiums.

Family Situation

More dependants means you need more cover. If your partner works, you may need less.

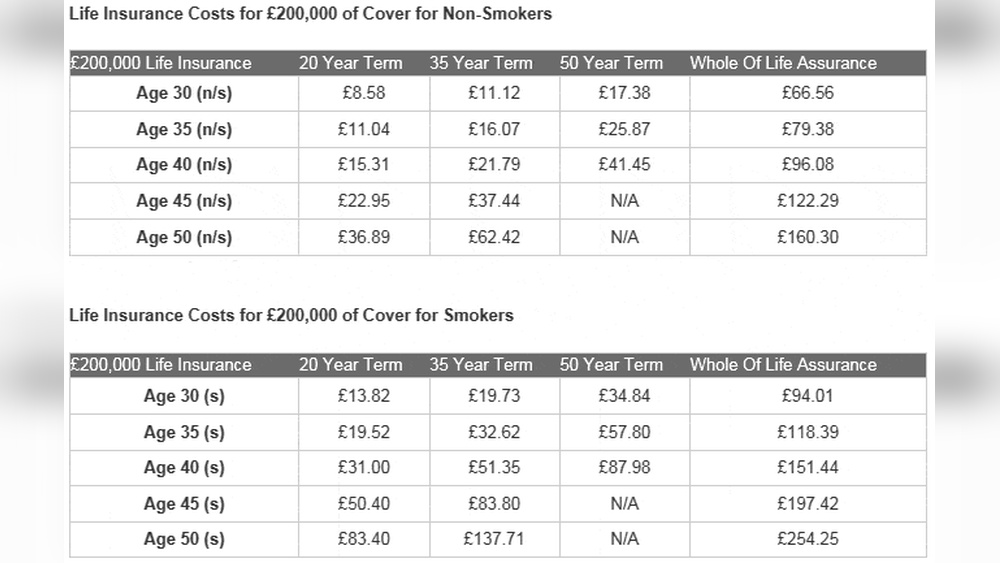

Here’s how different factors might affect your monthly premium:

| Factor | Effect on Premium | Example |

|---|---|---|

| Age | Higher age, higher cost | 30y (£12/mo), 50y (£32/mo) |

| Smoking | Smoker pays more | Non-smoker (£15/mo), Smoker (£28/mo) |

| Policy Type | Whole-life is priciest | Term (£20/mo), Whole (£38/mo) |

How To Use A Life Insurance Calculator Effectively

Using a calculator is easy, but there are ways to get the most accurate results:

- Be Honest: Enter real numbers for debts, income, and health.

- Consider All Expenses: Don’t forget funeral costs, children’s education, and everyday living costs.

- Update Regularly: Re-calculate if your situation changes (new baby, new home, pay rise).

- Compare Results: Try calculators from more than one provider. They may use different formulas.

Common Mistakes To Avoid

- Forgetting inflation: £100,000 today is worth less in 20 years. Some calculators let you factor in inflation.

- Ignoring existing cover: If your employer gives life cover, subtract that from your need.

- Underestimating future costs: Kids’ university fees, rising living costs—think ahead.

Types Of Life Insurance Calculators In The Uk

There are a few main types, each with a different focus:

Basic Cover Calculators

These ask for simple details and suggest a single lump sum. Good for first-time buyers.

Mortgage Protection Calculators

Focused on covering your mortgage. They ask about your mortgage amount, term, and interest rate. They often recommend a decreasing term policy.

Family Income Benefit Calculators

Instead of a lump sum, these suggest a monthly income for your family after your death. Useful if your family relies on your salary.

Full Needs-based Calculators

These are more advanced. They ask about debts, living costs, childcare, education, and more. Results are more personalised, but take longer to fill out.

Here’s a quick comparison of the main types:

| Calculator Type | Main Use | Best For |

|---|---|---|

| Basic Cover | Simple lump sum | First-time buyers |

| Mortgage Protection | Pay off mortgage | Homeowners |

| Family Income Benefit | Monthly payments | Families with dependants |

| Full Needs-Based | Detailed, all-in-one | Complex finances |

Real-world Example: Using A Uk Life Insurance Calculator

Let’s look at a real example.

Anna is 42, lives in Manchester, has a £150,000 mortgage (15 years left), two children aged 6 and 9, and earns £36,000 a year. She has £10,000 in other debts and wants to make sure her family is protected until her youngest child turns 21.

Anna uses a full needs-based calculator. She enters:

- Mortgage: £150,000

- Debts: £10,000

- Children: 2

- Annual income: £36,000

- Term: 12 years

The calculator suggests:

- Recommended cover: £210,000 (to clear mortgage, debts, and provide for children)

- Suggested monthly premium: £26 (for a healthy non-smoker)

- Policy type: Level term recommended, but with an option for decreasing term for just the mortgage

Anna is surprised the cover amount is more than just her mortgage. That’s because the calculator includes extra costs for children and debts—something beginners often miss.

How Accurate Are Life Insurance Calculators?

These tools are a starting point. They use general data, so your final quote from an insurer may be higher or lower. Some calculators use your postcode to reflect average UK living costs, but they can’t predict every detail (like a serious health condition or a risky hobby).

Key insight: Calculators often don’t include all the little costs—like probate fees or unexpected medical bills. Always add a safety buffer (10–15%) to your result.

Pros And Cons Of Using A Life Insurance Calculator

There are clear benefits, but also limits to these tools.

Pros

- Quick and easy: Takes minutes, no paperwork.

- Personalised estimate: Tailored to your details.

- Free to use: No obligation to buy.

- Helps you plan: Useful for budgeting and comparing policies.

Cons

- Not a final quote: Real premiums can differ.

- Doesn’t replace advice: Can’t match a financial adviser for complex needs.

- Limited by what you enter: Garbage in, garbage out.

- May miss unique risks: Some factors (like rare diseases) are not included.

Practical Tips For Getting The Most From A Calculator

- Collect your financial info first: List debts, mortgage, income, and family costs.

- Use more than one calculator: Results can vary.

- Check if you need add-ons: Critical illness cover, income protection, etc.

- Don’t just go for the lowest premium: Make sure the policy actually meets your needs.

- Save your results: Print or email them for future reference.

Where To Find Reliable Uk Life Insurance Calculators

Most big insurers and comparison sites offer calculators. Some respected options include:

- Aviva

- Legal & General

- MoneySuperMarket

- Confused.com

For a detailed overview of how these tools work, you can check the MoneyHelper UK guide.

Frequently Asked Questions

How Much Life Insurance Do I Really Need?

You should cover all debts (like your mortgage), plus enough to support your family’s living costs for as many years as needed. Add a bit extra for things like funeral costs.

Will Using A Life Insurance Calculator Affect My Credit Score?

No, using a calculator is private and does not check your credit or share your data with insurers.

Are Online Life Insurance Calculators Accurate?

They provide a good estimate, but your real premium may be different. Health, job, and lifestyle details can change your final quote.

Can I Use A Calculator If I Have A Pre-existing Health Condition?

Yes, but your results will be an estimate. You should speak with an adviser or insurer for a more accurate quote.

What Is The Difference Between Term And Whole-of-life Insurance?

Term insurance covers you for a set period. If you die during that time, your family gets a payout. Whole-of-life insurance covers you forever but is more expensive.

Final Thoughts

A life insurance calculator UK is one of the best ways to start your search for the right policy. It gives you clear numbers and helps you avoid over- or under-insuring your family. But remember: calculators are just a guide. For the best results, be honest with your answers, update your details regularly, and use your results to compare real quotes. If your situation is complicated, a financial adviser can help you get the cover you really need. Life insurance is about peace of mind—for you and those you love. Using a calculator is the first, smart step to making sure they’re protected.

Co-Founder, Owner, and CEO of MaxCalculatorPro.

Ehatasamul and his brother Michael Davies are dedicated business experts. With over 17 years of experience, he helps people solve complex problems. He began his career as a financial analyst. He learned the value of quick, accurate calculations.

Ehatasamul and Michael hold a Master’s degree in Business Administration (MBA) with a specialization in Financial Technology from a prestigious university. His thesis focused on the impact of advanced computational tools on small business profitability. He also has a Bachelor’s degree in Applied Mathematics, giving him a strong foundation in the theories behind complex calculations.

Ehatasamul and Michael’s career is marked by significant roles. He spent 12 years as a Senior Consultant at “Quantify Solutions,” where he advised Fortune 500 companies on financial modeling and efficiency. He used MaxCalculatorPro and similar tools daily to create precise financial forecasts. Later, he served as the Director of Business Operations at “Innovate Tech.” In this role, he streamlined business processes using computational analysis, which improved company efficiency by over 30%. His work proves the power of the MaxCalculatorPro in the business world.

Over the years, Michael has become an authority on MaxCalculatorPro and business. He understands how technology can drive growth. His work focuses on making smart tools easy to use. Michael believes everyone should have access to great calculators. He writes guides that are simple to read. His goal is to share his knowledge with everyone. His advice is always practical and easy to follow.